This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

This week, Im rerunning some popular posts while I prepare for Fridays Drug Channels Outlook 2025 live video webinar. During Friday's webinar, Ill share some updated thoughts on biosimilars and PBMs private label products. The Humira biosimilar market just took another step forwardbut remains far from its ideal state.

Biosimilars have emerged as a game-changing force, promising to revolutionize patient access to life-saving biologics while simultaneously reducing healthcare costs. ”[1] The global biosimilars market is experiencing exponential growth, with projections indicating it will reach $69.4 billion by 2025, growing at a CAGR of 34.2%

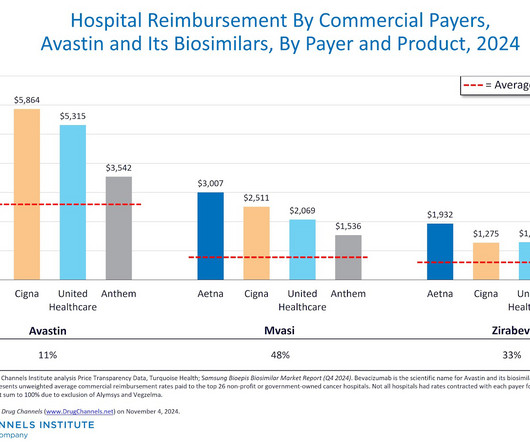

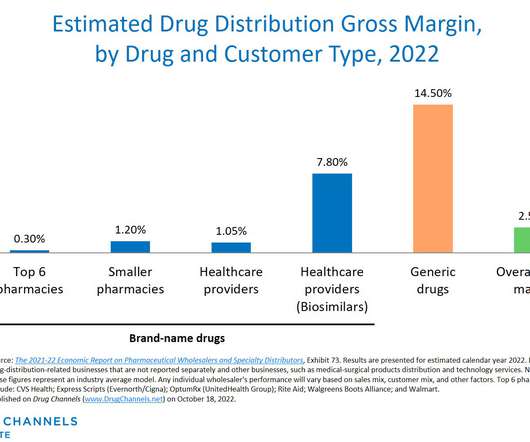

Here on Drug Channels , we have long highlighted the boom in provider-administered biosimilars. In contrast to the pharmacy market, adoption of these biosimilars is growing, prices are dropping, and formulary barriers continue to fall. As we demonstrate, health plans pay hospitals far above acquisition costs for biosimilars.

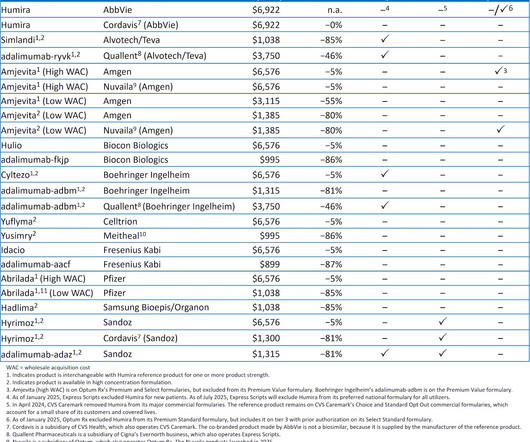

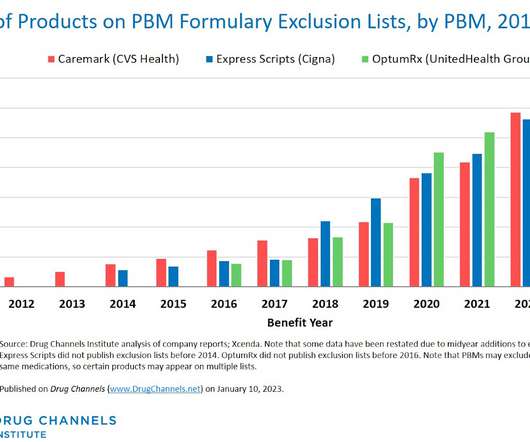

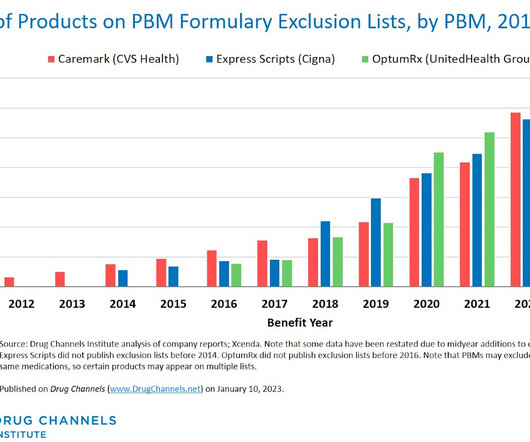

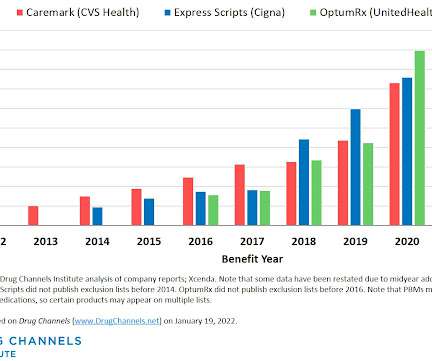

For 2025, the three largest pharmacy benefit managers (PBMs)Caremark (CVS Health), Express Scripts (Cigna), and Optum Rx (United Health Group)have again each excluded hundreds of drugs from their standard formularies. In fact, nearly all marketed Humira biosimilars are excluded from the larger PBMs 2025 formularies. What do you think?

Spring has officially arrived in sunny downtown Philadelphiathe proud home base of Drug Channels. As you can see on the right, we celebrated in Miami at the Drug Channels Leadership Forum. Read more 2006-2025 HMP Omnimedia, LLC d/b/a Drug Channels Institute , an HMP Global Company. Join Adam J. Fein, Ph.D., to 1:30 p.m.

The biosimilar boom for provider-administered drugs continues to accelerate. Net prices in therapeutic classes with biosimilar competition have declined by 60% or more over the past few years. Some major biological reference products have now lost a majority of their unit sales to their biosimilars. drug distribution.

As regular readers know, the biosimilar boom for provider-administered drugs has been accelerating. In many therapeutic areas, biosimilars’ market share is approaching 80%. That’s when Humira, the best-selling drug in the U.S., will face multiple biosimilar competitors. d/b/a Drug Channels Institute.

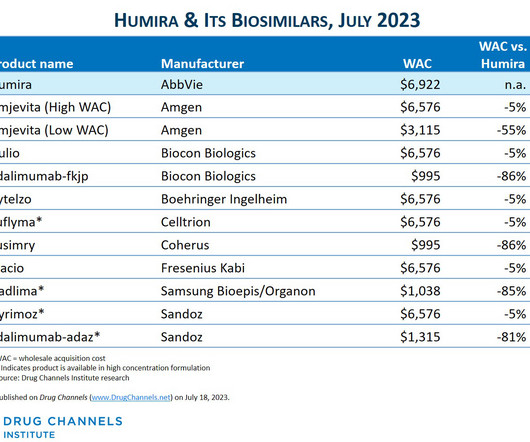

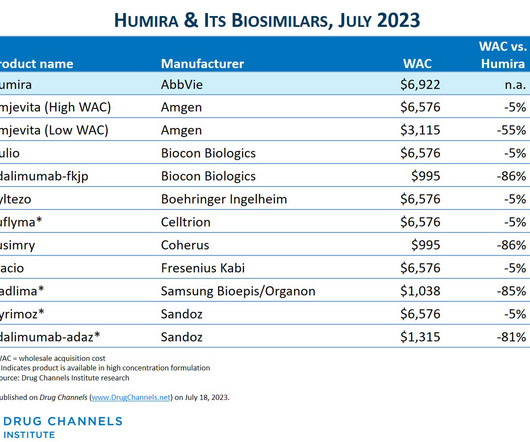

Since I published the article below in July 2023 , there have been three notable market develpoments: IQVIA has reported that as as of mid-2023, there was almost no adoption of Amgen's Amjevita, the first Humira biosimilar. Boehringer-Ingelheim launched an unbranded, low WAC version of its interchangeable biosimilar.

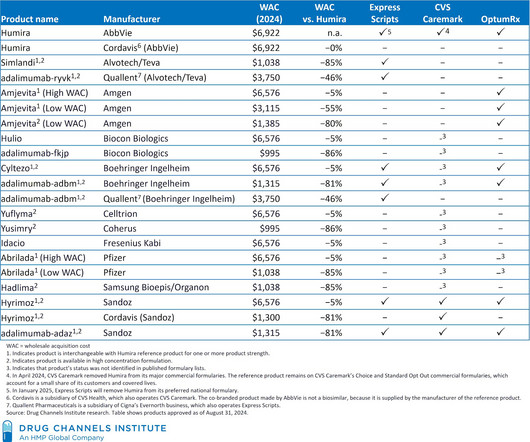

For 2024, the three largest pharmacy benefit managers (PBMs)—Caremark (CVS Health), Express Scripts (Cigna), and OptumRx (United Health Group)—have again each excluded 600 or more drugs from their standard formularies. This year, Humira and its 13 biosimilars will provide the most intriguing formulary drama. All rights reserved.

It's time for a super-sized Halloween roundup of wicked Drug Channels ’ tales. CVS Health frightens all but one Humira biosimilar maker away from its formulary. The gross-to-net bubble for anti-obesity GLP-1 drugs walks among us. Mark Cuban Cost Plus Drug Company conjures a partnership with Alto Pharmacy.

CVS Health has finally revealed its strategy for biosimilars of AbbVie’s Humira. Rather than announce multiple biosimilars for its pharmacy benefit manager (PBM) formulary, the company will instead launch Cordavis, a new subsidiary that will market a private label, low-list-price version of Sandoz’ Hyrimoz.

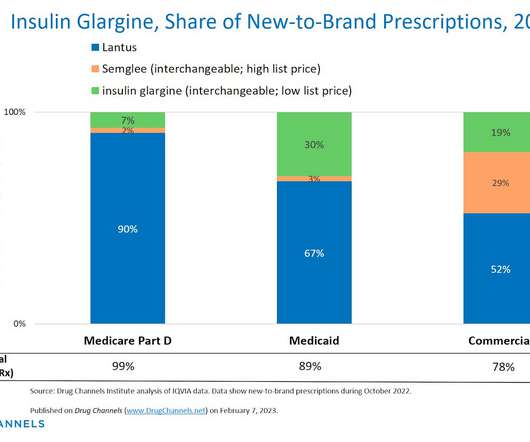

The Food & Drug Administration (FDA) recently approved the first interchangeable biosimilar insulin product: the insulin glargine-yfgn injection from Viatris. drug channel will limit the impact of this impressive breakthrough. Viatris is being forced to launch both a high-priced and a low-priced version of the biosimilar.

An ironic postcript: Less than two months after my article was published, Cigna CEO David Cordani bragged about the cost savings from "aggressive adoption" of biosimilars. Anyone want to tell him about the Express Scripts formulary for insulin biosimilars? drug channel will limit the impact of this impressive breakthrough.

While we wait for the Phillies turnaround, let’s oil up our gloves, lace up our cleats, and run the bases around this month's biggest hits: Foul ball : OptumRx prefers higher prices for the first Humira biosimilar Strikeout : Copay accumulators hurt health equity Bench warmer : Surprise? d/b/a Drug Channels Institute.

Along with sunshine and fine weather, this vernal equinox has ushered in a crop of new and noteworthy stories: Health inequities in utilization management Insurers compute big white bagging savings The biosimilar boom accelerates The patient upside of manufacturers’ copay support Whoa. d/b/a Drug Channels Institute. to 1:30 p.m.

The biosimilar market is finally beginning to fulfill its promise. The latest data show that provider-administered biosimilardrugs are successfully displacing their reference biological products. As I predicted last year, newer biosimilars are being adopted quickly, and their prices are declining rapidly.

This week, I’m rerunning some popular posts while I prepare for this Friday’s video webinar: Drug Channels Outlook 2021. Drug pricing perceptions always seem to lag reality. Conveniently for HHS, ASPE's analysis stopped before the biosimilar boom began. The biosimilar market is finally beginning to fulfill its promise.

Time to pack away the bathing suit and get serious again—with these curated curiosities combed from the now-barren Drug Channels beach: OptumRx joins the PBM GPO game Pharmacy DIR fees hit $11 billion A terrific resource on state biosimilar laws Patient views on utilization management Plus, my social media success…from a (print) newspaper ad!

We organize all of the trending information in your field so you don't have to. Join 15,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content